You’ve been writing code for six months. You and your co-founder have a product, a handful of early customers, and a pre-seed round behind you. An investor wants to meet next week and you know they’re going to ask about your financial model.

You don’t have one. You’re not even sure what goes in one.

This is a normal place to be. Most technical founders haven’t built a financial model before. The problem isn’t intelligence. It’s that startup finance has its own vocabulary and conventions, and nobody teaches them to you until someone asks for a spreadsheet you don’t have.

Here’s how to go from zero to a credible financial model in a single afternoon.

Start with what you already know

Open Burncast and enter your current team: two co-founders, their roles, their salaries. Then add the hires you’re planning: an engineer and a designer starting in a few months, an account executive after that. You don’t need to nail every detail. Start with what you know and refine later.

The Team page now also shows stacked trend charts above the table, so you can see how headcount and payroll evolve by category while you model.

Next, your revenue. You have a subscription product at $19,999 per year with annual billing. Revenue growth is sales-driven: link your subscription to the people who sell it (your CEO and account executive), set the number of deals each rep closes per year, and Burncast projects revenue based on headcount. As you hire more reps, revenue scales automatically. You can change these assumptions later without breaking anything.

The Revenue page shows stacked charts by source with an interactive legend, so you can quickly see which streams drive total revenue and active units over time.

Then your expenses beyond payroll. Cloud infrastructure, API costs, that coworking space. Monthly amounts, start dates, expected increases. Straightforward.

You’ve just described your business in numbers. Took maybe 20 minutes.

Model your funding round without a finance degree

Here’s where most founders get stuck in spreadsheets. Funding rounds involve terms like pre-money valuation, dilution, and price per share, and they’re all different ways of saying related things.

Burncast lets you enter a funding round however you think about it. If your investor said “we’ll put in $1M at a $5M pre-money valuation,” enter it that way. The cap table (the ownership breakdown of your company) gets calculated from there.

You don’t need to work out the dilution yourself. Burncast figures it out: $1M at a $5M pre-money means roughly 17% dilution. It’s shown to you, in context, so you learn by doing.

The inline glossary changes everything

Every financial term in Burncast is explained where you encounter it. Hover over “burn rate” and you see: the amount of cash your company spends each month beyond what it earns. No switching to Google. No pretending you know what a term means during a board meeting.

After an afternoon of building your model, you’ll have picked up 10-15 finance terms through context. Not from a textbook. From seeing them applied to your own numbers.

Your model generates the hard stuff

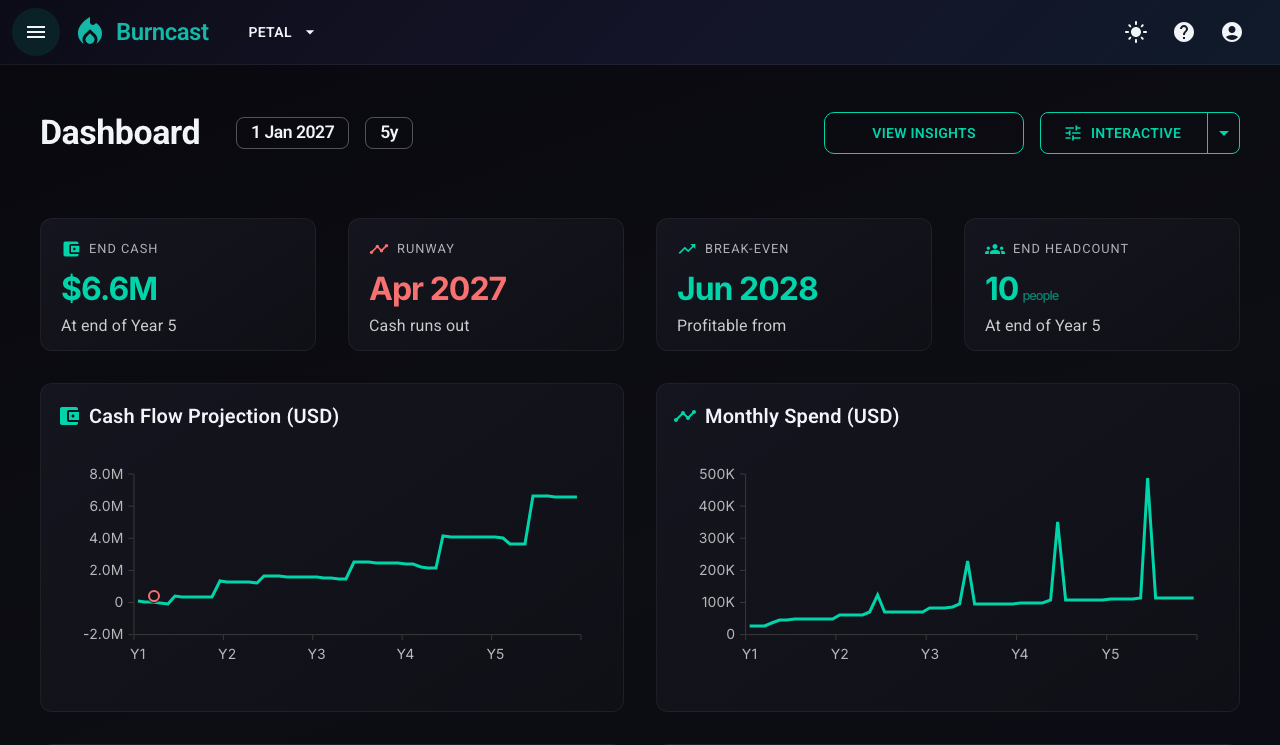

Once your assumptions are in, Burncast produces the outputs investors actually want to see. The dashboard at the top of this post shows the projections: runway, burn rate, and revenue charts generated from your inputs.

The annual income statement lays it all out in one table: revenue, costs, margins, and net income for each year. This is the format investors and board members expect to see. You can also switch statement headings between Calendar, Model, and Both modes, depending on how you want to present periods.

The cap table tracks who owns what, before and after each round. Founders, investors, option pool, all laid out, with dilution calculated automatically as rounds close.

You didn’t write a single formula. You didn’t copy a template from someone’s blog and hope the cell references were right.

Now ask the real question: what if you raise more and hire faster?

Create a second scenario. In Burncast, a scenario starts as a copy of your base model, but you only change what’s different. This is difference-based modeling, where each scenario stores just the differences, not a whole separate model.

Raise the round from $1M to $1.5M at a $6M pre-money. Hire more aggressively: extra engineers, a sales rep. Bump your growth assumptions to match.

Now compare. The larger round gives you more runway and faster growth, but costs you more ownership. The conservative round preserves equity but leaves less room for error.

That’s a real conversation to have with your co-founder. And you can have it with actual numbers, not guesses.

What you walk away with

In one afternoon, you built a financial model, learned the vocabulary investors use, and ran two funding scenarios. You’re walking into that investor meeting with projections you understand, because you built them from your own assumptions, not from a spreadsheet someone else made.

That’s the point. A financial model isn’t a document you produce for someone else. It’s a tool for thinking about your business. And now you have one.